When it comes to protecting your family’s financial future, Insurance Brokers, like myself, are invaluable allies. A good broker will go beyond basic insurance policies to offer a range of supplemental benefits tailored to meet specific needs and ensuring your family’s financial security involves more than just minimal coverage.

I offer a variety of supplemental benefits tailored to meet specific needs. Let’s dive into the key types of supplemental benefits available:

1. Life Insurance:

Life insurance is crucial for families to protect against financial hardship in the event of a primary breadwinner’s death. It provides a lump-sum payment (death benefit) to beneficiaries, ensuring they can maintain their standard of living and cover expenses.

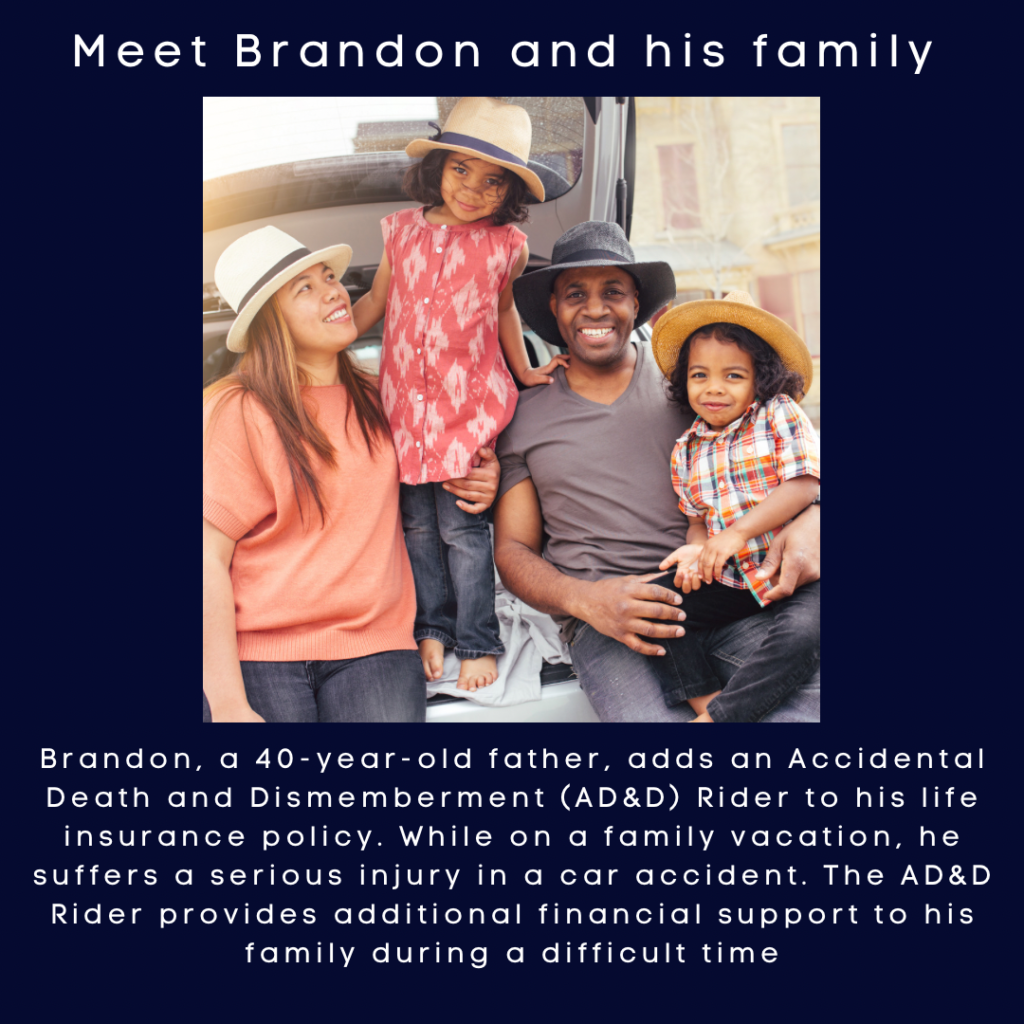

Life Insurance: Life insurance is more than just a death benefit; it can also provide financial security during critical moments. Insurance brokers offer riders that enhance standard life insurance policies, such as: Accidental Death and Dismemberment (AD&D): AD&D coverage provides additional benefits if death or serious injury occurs due to an accident. It ensures financial support for unexpected tragedies.

Let’s make a real life connection by taking a look at a scenario:

2. Critical Illness Insurance:

Critical illness insurance pays out a lump sum if the policyholder is diagnosed with a covered critical illness (e.g., cancer, stroke). This benefit helps cover medical costs, allows for lifestyle adjustments, and provides financial support during recovery.

Critical Illness: This rider pays out a lump sum if the insured is diagnosed with a critical illness like cancer, heart attack, or stroke. It helps cover medical expenses and other financial obligations during recovery.

Let’s make a real life connection by taking a look at a scenario:

3. Disability Insurance:

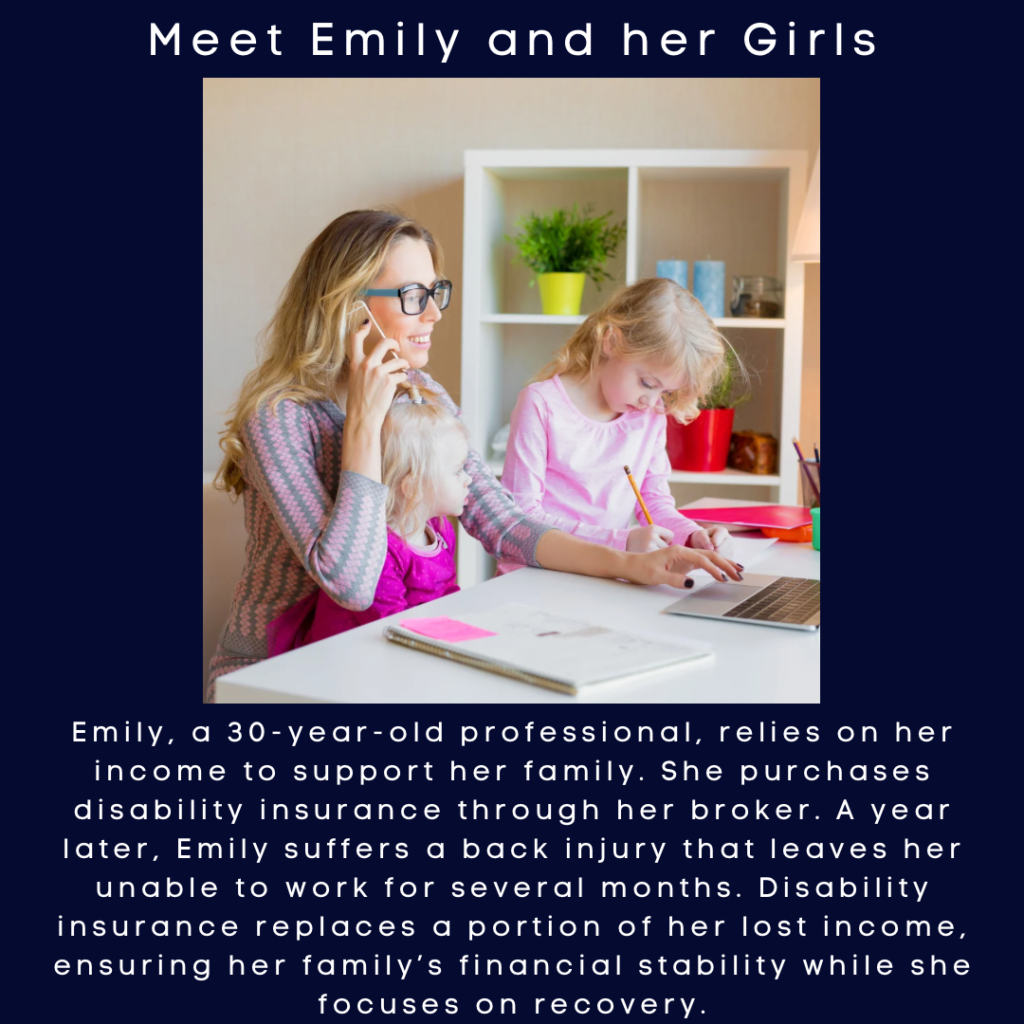

Disability insurance provides income replacement if the insured becomes unable to work due to illness or injury. It ensures families can continue to meet financial obligations, such as mortgage payments, utilities, and daily expenses.

Disability insurance provides income replacement if the insured person becomes disabled and unable to work. It ensures financial stability by replacing a portion of lost income, helping families maintain their standard of living.

Let’s make a real life connection by taking a look at a scenario:

4. Long-Term Care Insurance:

Long-term care insurance covers the cost of care in a nursing home, assisted living facility, or at home if the insured requires assistance with expenses associated with extended medical and personal care services with activities of daily living due to aging, illness, or injury. It eases the financial burden on families during challenging times. It may include:

Home Care Service: Assistance with daily activities at home, such as nursing care and help with personal hygiene.

Nursing Home Care: Coverage for stays in a nursing home or assisted living facility, ensuring quality care without exhausting savings.

Waiver of Premium: If the policyholder becomes disabled and unable to work, this rider waives premium payments while maintaining coverage. It eases financial strain during periods of incapacity

Let’s make a real life connection by taking a look at a scenario:

5. Travel Insurance:

Travel insurance provides coverage for medical emergencies, trip cancellation, lost baggage, and other unexpected events while traveling outside Canada. It offers peace of mind and financial protection during vacations or business trips.

Navigating these supplemental benefits requires careful consideration of your family’s unique needs, financial situation, and risk tolerance. Insurance brokers play a crucial role in assessing these factors and recommending tailored solutions to protect your family’s financial well-being.

Travel insurance is essential for families traveling outside Canada. It provides coverage for:

Medical Emergencies: Covers medical treatment, hospital stays, and emergency medical evacuation.

Trip Cancellation: Reimburses prepaid expenses if a trip is canceled or interrupted due to covered reasons.

Lost Baggage: Provides compensation for lost, stolen, or damaged luggage and personal belongings.

Let’s make a real life connection by taking a look at a scenario:

6. Supplementary Health Benefits:

Includes services like paramedical practitioners (e.g., chiropractors, physiotherapists) and medical equipment not covered under provincial plans.

Supplementary health benefits include services not fully covered by provincial health plans, such as:

Paramedical Practitioner: Coverage for services from chiropractors, physiotherapists, massage therapists, and psychologists.

Medical Equipment: Reimbursement for the cost of durable medical equipment like wheelchairs, walkers, and prosthetics.

Let’s make a real life connection by taking a look at a scenario:

Navigating these supplemental benefits can be complex, but someone like myself can simplify the process by providing expert and personalized advice and to explore the full range of supplemental benefits available.I will guide you to make informed decisions that meet your family’s specific needs and budget by assessing your needs and finding the right solutions to safeguard your family’s future.

Call, ask for Cheryl and schedule a virtual intake session today!

Find out what’s best for you family

I’m here to help. Let’s talk.

-

Understanding the Different Types of Supplemental Health Benefits Available In Canada

When it comes to protecting your family’s financial future, Insurance Brokers, like myself, are invaluable allies. A good broker will go beyond basic insurance policies to offer a range…

4 min read

-

Canadian Families Are Realizing The Importance of Supplemental Benefits!

Securing Your Family’s Future: The Importance of Supplemental Benefits for Canadian Families: A Comprehensive Guide In today’s uncertain world, ensuring the health and well-being of our loved ones…

4 min read